30 Aug 2021

CFTC Positioning Report: Net longs in EUR extended the downtrend

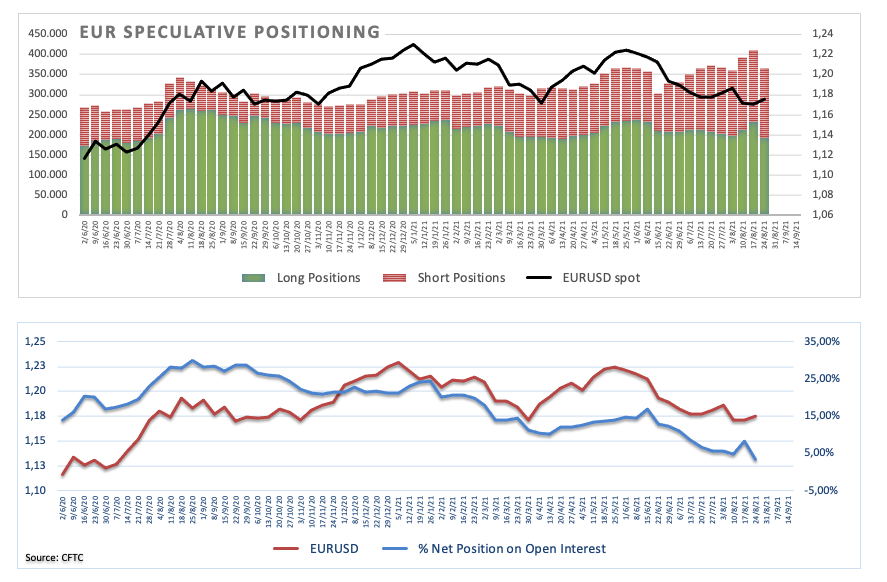

These are the main highlights of the CFTC Positioning Report for the week ended on August 24th:

- Speculators moderately trimmed their gross longs in the euro, reversing the previous uptick and dragging net longs to the lowest level so far this year and, at the same time, re-visiting figures last seen in late September 2018. In addition, net position on open interest dropped to levels just above 3%. Initial strength in the dollar during the period under study weighed on the risk complex and forced EUR/USD to record new 2021 lows near 1.1660, just to rebound afterwards on the back of a potential disappointment at the Jackson Hole Symposium.

- The opposite path followed the dollar after net longs climbed to levels last seen in early March 2020, the onset of the coronavirus pandemic. Bouts of risk aversion propped-up by the progress of the delta variant and speculations on an anticipated tapering talk gave legs to the dollar and pushed the US Dollar Index (DXY) to the 93.70 zone, levels last traded back in November 2020. The subsequent move lower in DXY was pari passu with rising rumours that Chief Powell could keep the cautious tone at the Jackson Hole event (after the cut-off date).

- The sterling returned to the negative territory after two weeks in a row, with net shorts reaching late November 2020 levels. Cable retreated to the vicinity of the 1.3600 yardstick amidst the firmer dollar, managing to regain traction afterwards.

- The speculative community remains negatively positioned on AUD, as net shorts escalated to the area of early September 2019. Persistent restrictions in response to COVID-19 jitters plus some loss of momentum around Chinese growth prospects kept the Aussie dollar well under pressure.

- In the safe haven universe, CHF net longs receded to nearly 3-month lows while net shorts in JPY went up levels last seen in early July.

- Prices of the WTI remained depressed and extended the corrective downside to the sub-$62.00 mark, just to rebound sharply on Monday and Tuesday. The progress of the delta variant and its impact on the global recovery and demand for crude oil coupled with the strong dollar added to the sharp correction from August highs near the $74.00 mark per barrel.